Canadian agriculture’s business environment seems even more uncertain than usual. Markets are more volatile than historically. President Trump seems bent on causing new uncertainties in, among other areas, international trade.

As this is written, it is not completely certain that Canada will remain in NAFTA, or exactly what shape that agreement will take. Meanwhile, the Canadian government also creates uncertainty about investment in the energy sector, which can impact labour markets.

Always uncertain, weather appears to be even more so in recent years with risks at your farm, but also on prices because of weather in competitor countries. And, of course, there are all the things that can go wrong at the individual farm level from accidents and the loss of key people to crop and livestock diseases, equipment failures and the like.

Read Also

What producers need to know about Health Canada’s latest food additive, enzyme and supplement updates

Changes to Health Canada’s food additive, enzyme and supplement regulations influence how raw and processed agricultural products can be marketed, labelled and formulated across the value chain.

Not everyone is comfortable with risk. The author has witnessed advisers to boards of publicly traded companies who like to look at every risk as unacceptable and forget that entrepreneurs, by definition, take risks.

The question is which risks should be taken and which should be managed?

Fortunately, there is a widely accepted and logical framework for identifying, assessing and choosing what to manage.

The risk assessment process

This is a three-step process that is a variant of strategic planning. The difference is subtle. When developing strategy we look for opportunities and how we can capitalize on them. In risk assessment, we look at threats: what can go wrong, and how do we deal with it if it does?

At the limit, however, these two processes converge: risk management is part of strategy.

Your first step is to identify as many potentially risky events as possible. In doing so we suggest examining separately the external and internal environments of your farm business. External events are things beyond your control, such as weather, changes in markets, unexpected changes in government policy, new diseases, actions taken by competitors to improve their competitive position, etc.

To approach the external environment logically, we suggest dividing it into four components:

- Policies, laws and regulations: these can be changes in environmental policy, pesticide or animal welfare regulations, trade policy, safety nets, etc.

- Socio-economic factors: e.g. consumer concerns about your production practices, changes in ethnicity.

- Competitors: other farmers can be competitors if, for example, they do something to drive their costs down, compete for land, or have advantages in other countries.

- Markets and customers: these factors include anything from declines in commodity prices to loss of an important customer who switches to another supplier(s) or experiences financial difficulty.

The internal environment includes factors you control with your management decisions. They also fall into four categories:

- People: this includes death or serious illness of a key person; a key employee quitting; loss of support of key management in a related company; divorce; or family feuding over any number of things that families feud over, especially in succession planning.

- Assets: this encompasses fire, property damage, hail, important off-farm investments.

- Finance: this requires understanding your financial position, especially debt service capacity, and it interacts with both production and markets.

- Processes: business process encompasses all the activities from obtaining inputs to delivering and collecting on final products. Risks then include the possibility of breakdown, sabotage, or becoming outdated.

After identifying possible risky events in each internal and external category, the second step is to estimate the impact each would have on the business and how likely it is to occur. This is crucial: overestimating means everything needs managing while understating means nothing does.

It’s also difficult to estimate the effects and likelihoods of things that may occur, but never have. There’s little data, for instance, on which to base calculations about off-the-wall trade policies by a U.S. president!

Two points are important for estimating impacts. First, we must understand our financials, as we have discussed in previous articles in Country Guide. It is essential that you know your historical and budgeted revenues, costs, operating and net profits as well as debt service requirements. For an event that can affect revenue or costs, estimating how much and how it will affect your ability to service debt gives great insight into how serious the event is to your business.

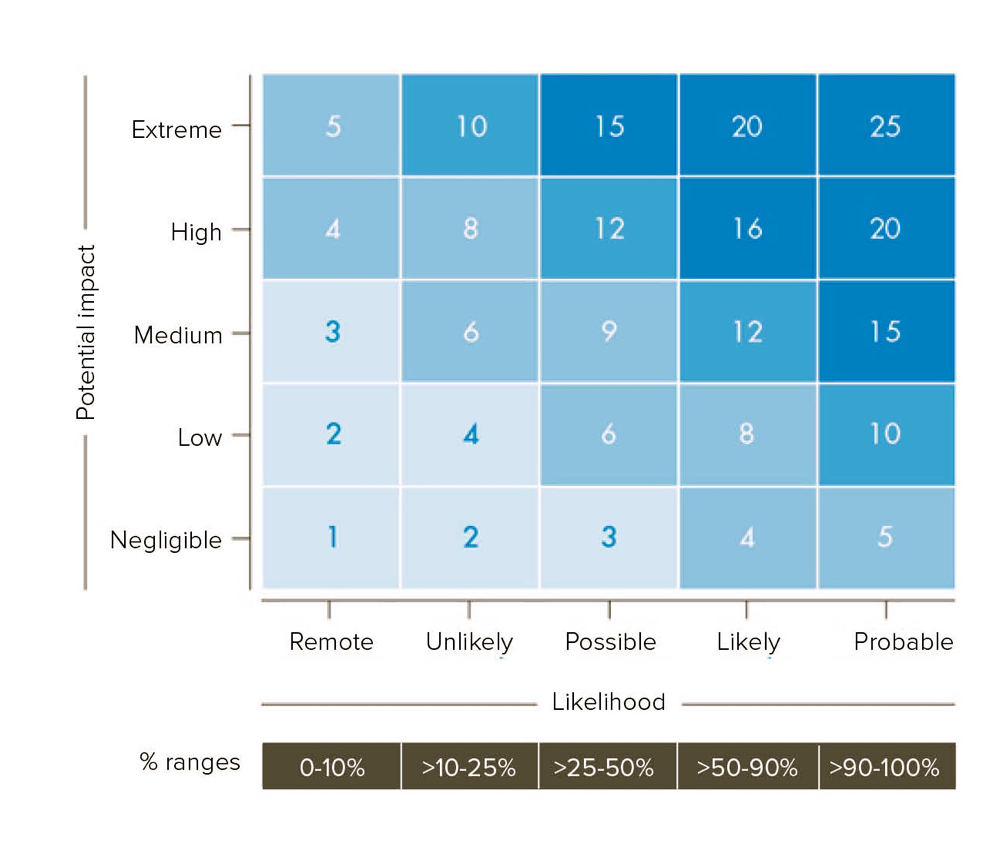

The second point is that whether or not it’s possible to put hard numbers on the consequence of an event, it’s still useful to make objective estimates. We like a five-category classification as shown in the diagram, with remote to probable for the likelihood of occurrence, and negligible to extreme for the impact.

A quite visual final step is to assign each potential event a code and to array them on the “heat chart,” where events upward to the right are the highest risk and, therefore, the ones that most need managing. While some events will be common to many farms, yours will be unique because of the industry you are in, your financial structure and your attitude toward risk.

Managing the risk

Of course, the challenge is deciding how to manage the risks. Some are best handled with insurance. Many can be done with prevention, i.e. having standard operating procedures in place that mitigate against things like accidents. An excellent risk management tool is the “because I love you” list developed for the surviving family members in case of sudden death. Many risks are best handled by managing costs and/or diversification along with conservative debt management.

Forward contracts and/or options can provide great assurance for many events that can affect prices. For example, November soybean prices have dropped from over US$10.50 per bushel to US$8.50 largely due to Trump’s trade policy. But they were $10 to $10.50 for four months before the crash. The loss could have been avoided.

Obviously not all risks can be identified or managed. But identifying your key risks and having a plan will facilitate a good night’s sleep!

Larry Martin is a principal in Agri-Food Management Excellence, which runs the Canadian Total Excellence in Agricultural Management (CTEAM) program.