It’s a question farm business advisors are hearing more and more from farmers across the country. “What can I do today to improve my financial position in five years?”

While there are a number of reasons why seeking out this type of advice is a good idea, management consultants Gavin Betker and Jacqueline Gerrard find the question often comes when business performance is mediocre and the farm team wants to move the mark. In other words, they’re surviving, but want to be thriving.

“It’s very common to hear that the farm is doing okay but they want to be better positioned because a challenge or opportunity is coming their way in a few years,” says Gerrard, who works with Betker at Backswath Management in Winnipeg, Man.

Read Also

Farm & Family – March 20 edition

As part of our International Year of the Woman Farmer content, we recently introduced readers to Renee Ardill, the third…

It’s one thing to say you want to improve your farm’s financial situation, but how would you actually do that? Where do you start? Betker and Gerrard recommend a three-step process to effectively analyze financial performance and create a customized action plan.

To illustrate this, Country Guide andthe team at Backswath Management have worked together on a case study example. The farm is fictitious, but Prairie Farm Ltd.’s financial information (see ‘CASE STUDY’ at bottom) is based on a real Canadian farm with real-life challenges — the kind of challenges that are common among many farm families.

For our online readers, additional charts with financial information on Prairie Farm Ltd can be found at the links below (provided by Backswath Management):

1. Where are you now?

“The first step is to find out how the operation is running right now, including who is involved, what is being produced and how the business is doing financially,” says Gerrard.

This involves a thorough analysis of the last five years of financial statements and using the data to calculate key financial ratios, including those defined below.

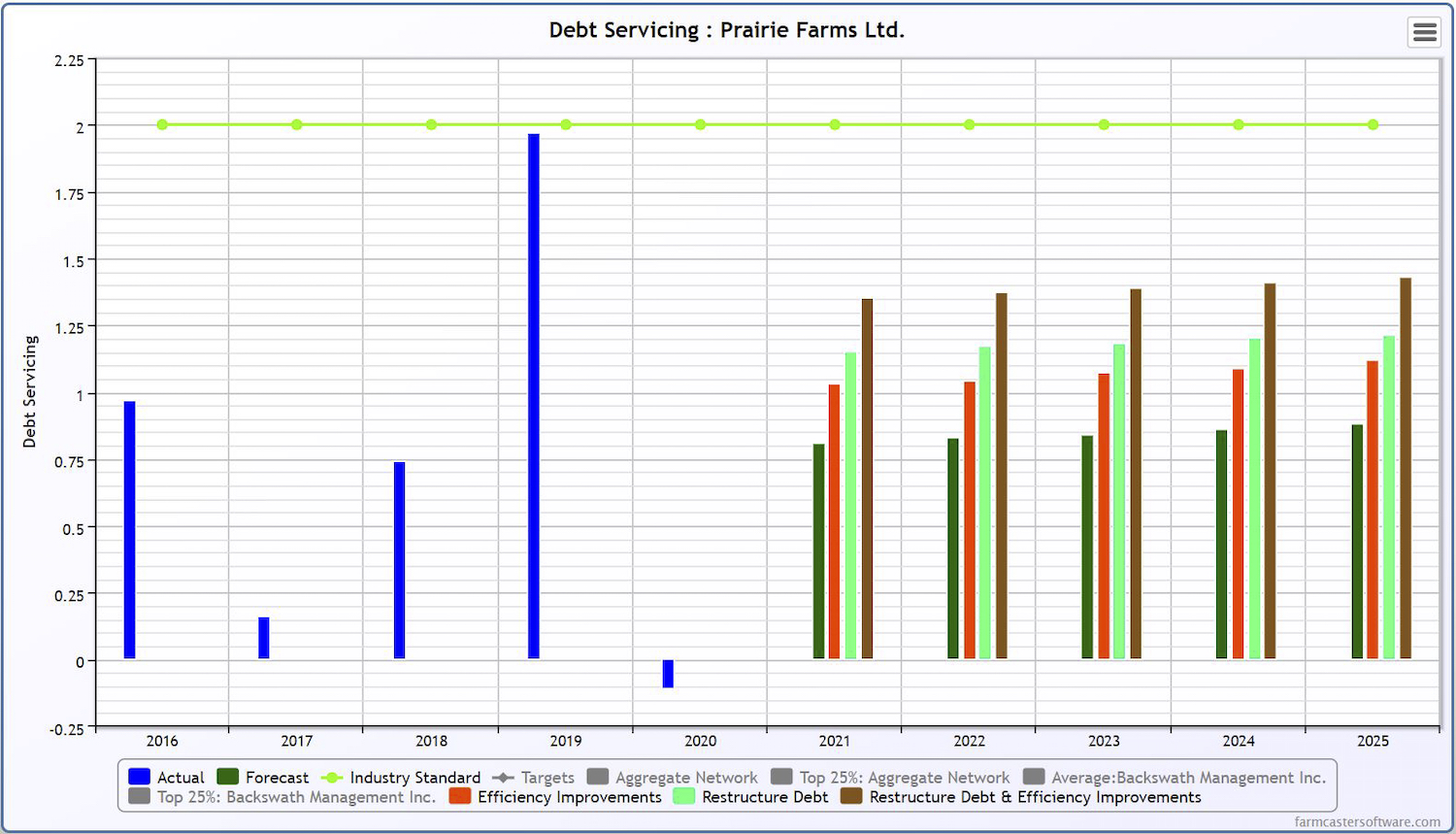

- Debt servicing is calculated by dividing debt servicing capacity by annual principal and interest payment commitments. Debt servicing capacity is calculated by adding amortization and long-term interest expense to net income. This ratio indicates the operation’s ability to repay debt.

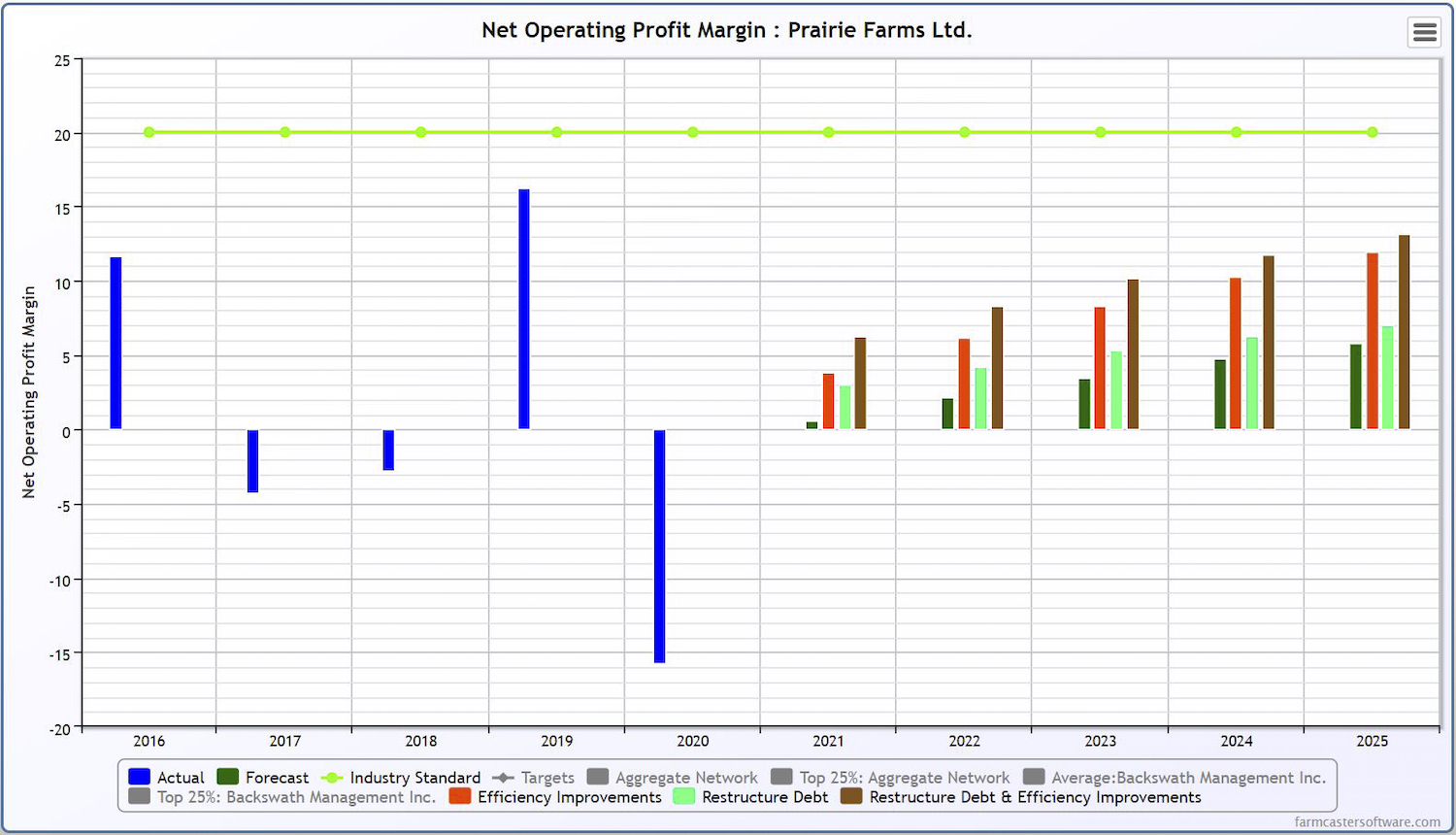

- Net operating profit margin is calculated by subtracting all costs, both fixed and variable, from the gross revenue to find the net operating profit. The ratio is calculated by then dividing net operating profit by gross revenue. It indicates how efficient a farm is at generating profit from operations, given all costs within the business. A higher percentage indicates better performance.

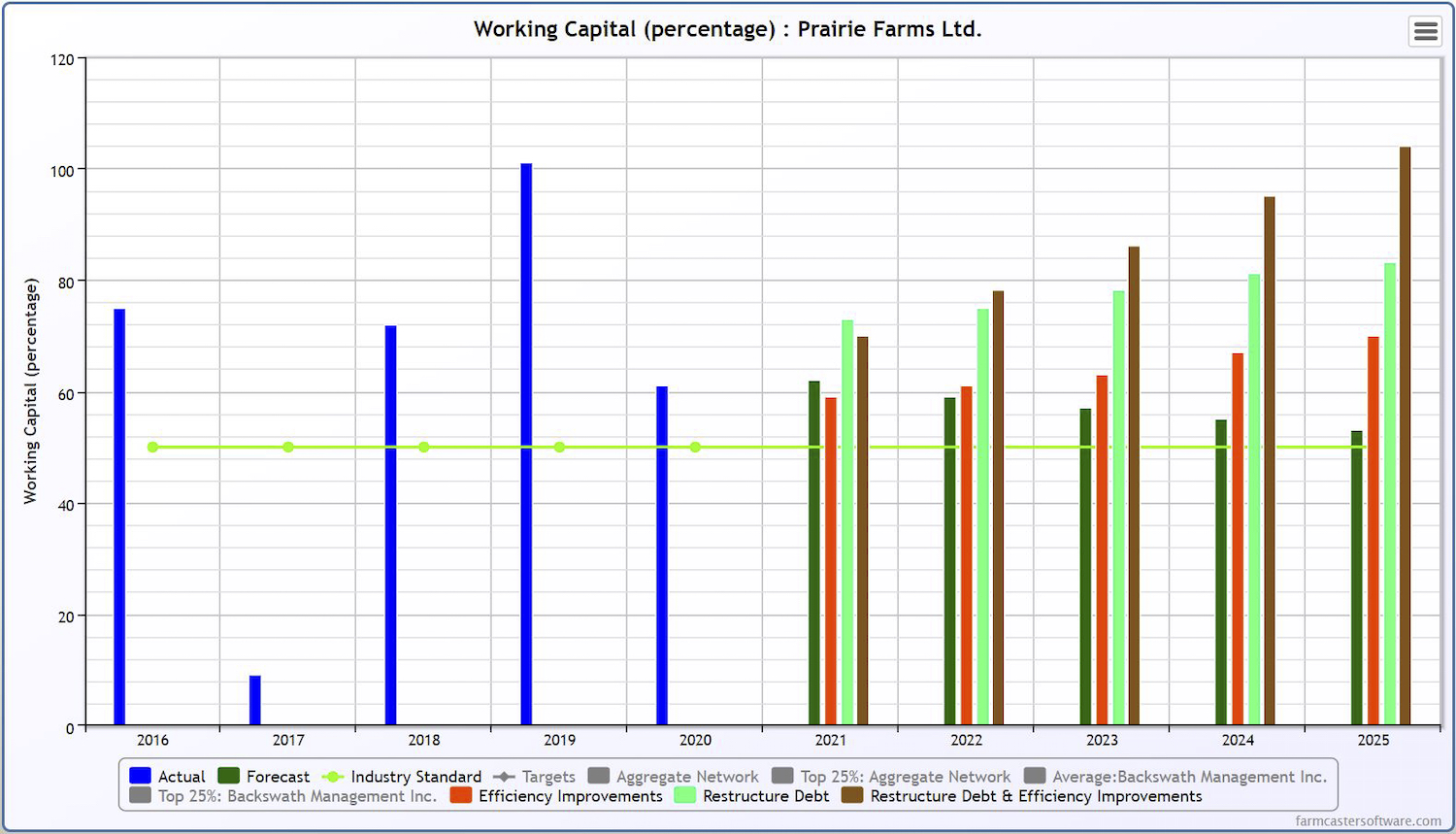

- Working capital is calculated by subtracting current liabilities from current assets. The result is the surplus or deficiency of current assets available to meet the current obligations of the business over the upcoming year. Working capital as a percentage of expenses is calculated by dividing the available working capital by the year’s cash expenses. A higher percentage indicates better performance.

The next step is to compare the ratios to industry benchmarks. While this may be hard for someone tackling this process on their own, determining how your data stacks up against others is key to assessing your position. Reaching out to an accountant, lender or other farm advisor to obtain benchmark averages can help.

“We look at what areas are strong or above the benchmark and what ratios are lower than average,” explains Gerrard. She then dives into the areas with room for improvement and talks with the client to find out the “why” behind the current figures.

Betker often finds farmers have a sense of where they need to improve, even before the ratios are calculated. It’s less about being a consultant who serves solutions on a platter and more about providing clients with analysis and context so they can make informed decisions, he says.

2. What are you working towards?

It’s also important to discuss and define where the business is headed.

While there may be an event coming down the pipe that managers want to prepare for, like, for instance, the intergenerational transition of Prairie Farms Ltd., Betker has noticed more and more farmers are starting this process proactively.

“There’s an overhanging cloud of uncertainty in farming that makes some managers want to better position themselves to take advantage of the next opportunity or sustain the next challenge, whether they know what that is or not,” says Betker.

Gerrard finds most clients can describe where they want their business to be in five or 10 years. It’s important to document this vision, though, and to ensure shorter-term goals are in alignment.

3. How can you get there?

From debt restructuring to diversification, there is a laundry list of strategies that can be considered when you look at where you want to get to from where you are now. Betker stresses that every business is unique and farmers should only implement the ones that make sense in their situation.

By combining the financial analysis completed in the first step with the future vision described in step two, the foundation is laid for the final task of crafting and selecting an action plan.

In the example of Prairie Farms Ltd., debt servicing is a concern so a debt restructuring makes sense.

In this case, Dad has been focused on doing whatever he can to keep long-term debt levels low. This mindset isn’t uncommon among farm business owners.

The common perception is that debt needs to be paid off. But while that’s true, Betker says trying to pay it off too quickly comes with disadvantages. He often talks with his clients about shifting their thinking to not only improve their financial position, but also reduce the stress and anxiety that can come with tight cash flow.

“Using other people’s money to help you make more money on your farm is a good thing,” Betker says. “We are lucky to be farming in Canada where there is a stable banking system and low interest rates right now.”

In the study, the cost of maintaining older equipment and the amount of wages being paid out were flagged as concerns during the financial analysis of the farm. That’s why Betker and Gerrard’s second recommendation hones in on new strategies to manage those specific expenses.

“Replacing equipment or adjusting family compensation could actually be tough decisions for some families to face,” explains Gerrard, noting that running older equipment may be a source of pride for some family members and paying adult children may be a difficult topic for Mom and Dad to bring up.

It is important to project the financial impacts of the recommendations over five years, since this makes it easy to see how making these changes now could better the business going forward.

The timeline of the impact depends on the strategy itself. It takes three to five years to make significant changes to the balance sheet of an average grain farm, but upgrading equipment, for example, can improve efficiency right away.

The moral of the story

Prairie Farms Ltd. could continue on the path it’s on and survive. Sure, there will be new challenges when the son and daughter enter the business, but the key financial ratios are forecast to come in at or just below industry averages for the next five years.

If they adopt and continue with the recommendations, however, the farm’s financial position is projected to improve significantly by 2027.

It’s a concept that can be applied to any business, he says. Experience shows that no set of farm financial statements is perfect. No matter how profitable the farm, there’s always something that can be improved. The goal, then, is to develop a process to identify the best changes and to forecast and then monitor what you can expect from them.

CASE STUDY: Prairie Farms Ltd.

Located in central Saskatchewan, Prairie Farms Ltd. is a multi-generation 5,000-acre grain farm. The farm is owned and managed by Mom and Dad, who have a son and daughter currently pursuing post-secondary education in agriculture. While both children have worked on the farm part-time for many years, the son will be returning to the business full-time after graduation next year and the daughter plans to follow suit in 2025.

Beginning position

This family values a hard day’s work and is proud to continue farming land that has been in Dad’s family for over 100 years.

From a management perspective, Mom and Dad do not have a written business plan. Dad usually makes business decisions in the moment and is focused on deferring capital purchases to keep long-term debt levels low.

Financial analysis of the past five years indicates an average gross revenue of $390 per acre. Average financial efficiency ratios correlate with average production efficiencies. Equipment assets are old and fully depreciated and there is little evidence of equipment reinvestment. Repairs and maintenance expense as well as wages stand out as being significantly higher than average. Loans are being repaid as agreed but there is often just enough money in the account to make debt payments.

- Debt Servicing: 0.88:1

- Working Capital: 53%

- Net operating profit margin: 5.8%

Strategic drivers

The need to generate additional revenue to support the children’s entry into the business and future intergenerational transition are key drivers for Prairie Farms Ltd. The business will change significantly after the son and daughter return from school and all family members acknowledge that it is not ready. What can they do to improve their financial position over the next five years?

Recommendation 1: Debt restructuring

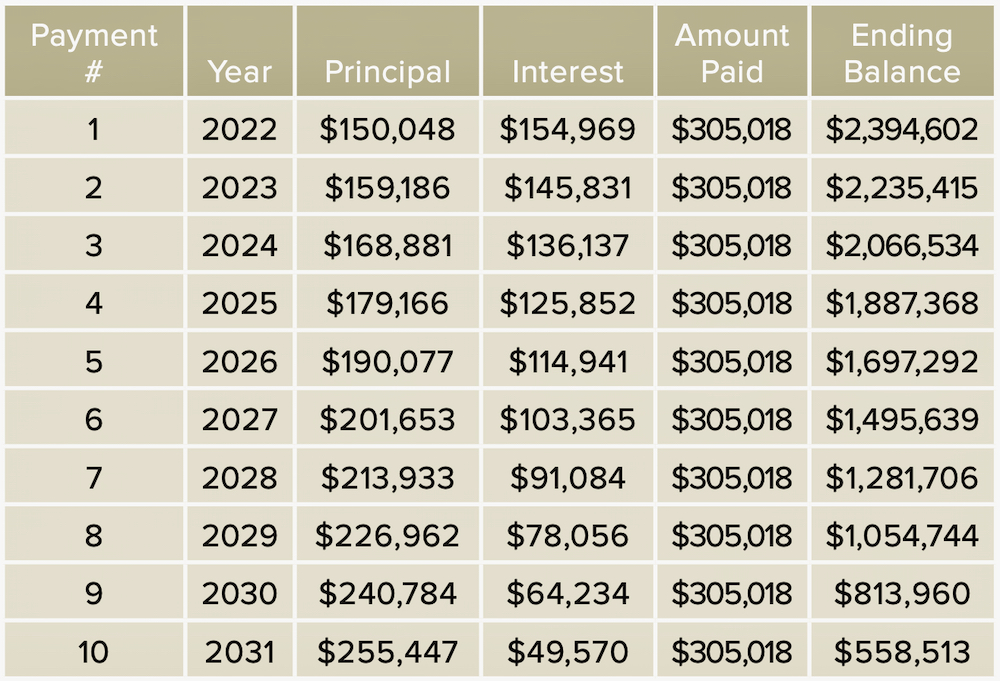

The farm’s debt totals $2,544,650 and is currently financed over 12 years at 6%. The annual payment is $305,017 and the current portion of long-term debt (principal) is $150,048 next year. (see above)

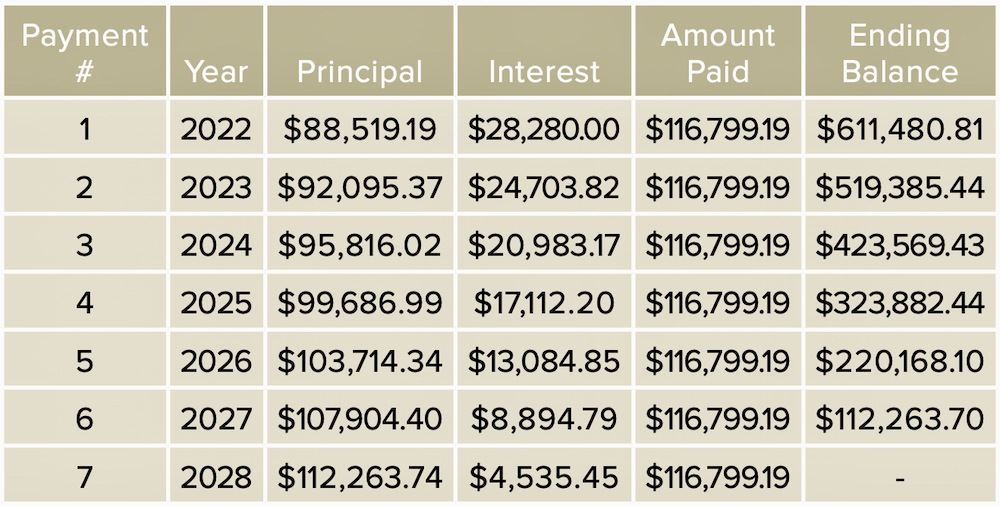

By extending the repayment term and shopping the interest rate with multiple lenders, the existing debt could be restructured over 20 years at 4%. The annual payment would be $187,903 and the current portion of long-term debt (principal) would be $85,100 next year (see below).

Why it matters: This debt restructuring immediately improves the financial position of the business, with a debt servicing surplus of $35,000 in the first year. This amounts to $175,000 in extra cash over the next five years.

- Debt Servicing: 1.2:1

- Working Capital: 83%

- Net operating profit margin: 7%

Recommendation 2: Efficiency improvements

Part 1: Equipment upgrades

Prairie Farms Ltd. currently owns a collection of older equipment, including a seed drill and 4WD tractor. Their average repairs and maintenance expense is $112,000. They lease two combines, valued at $800,000 together, and make payments of $115,000 annually. A local custom operator is hired for spraying, an expense that averages $40,000 annually.

An opportunity to improve efficiency lies in upgrading existing equipment and adding a sprayer to their lineup. The farm could sell $300,000 worth of existing equipment and purchase $1,000,000 in newer machinery — a drill ($350,000), 4WD tractor ($250,000) and sprayer ($400,000).

The financial difference is $700,000, which the farm could borrow over 7 years at 4% (see below).

Part 2: HR adjustments

Prairie Farms Ltd. is currently reporting annual operating wages of $200,650 and management salaries of $80,000. Wages include the amount paid to one full-time and two part-time employees. Mom, son and daughter are also paid seasonally. The management wages are paid to Mom and Dad. Son and daughter are currently paid based on their university and living costs.

Since the son and daughter’s pay does not currently reflect their contributions to the farm, a conversation could be had about what their compensation is going to look like going forward. After graduation, the children will join the business full-time but their current pay could be maintained. They would then be working to earn the money that they have been making. The son could take on spraying responsibilities utilizing their new equipment.

Why it matters: While this equipment upgrade does add to the farm’s debt load, it is projected to improve efficiency by 5%, representing $135,000 in revenue annually. Repairs and maintenance expense would decrease by approximately 20% ($22,400) and custom work expense would be reduced by approximately $40,000. The improved efficiency and decreased expenses more than covers the cost of borrowing for this upgrade.

As the son and daughter come home full-time, the family has enough HR capacity to replace the custom work. By maintaining their current wage, the farm becomes more efficient through better utilization of their labour.

- Debt Servicing: 1.12:1

- Working Capital: 70%

- Net operating profit margin 12%

Recommendations 1 and 2

If Prairie Farms Ltd. implements both of the above recommendations, their overall financial position improves significantly. The restructuring and improved efficiency strengthens debt service capacity right away and no new debt is projected in the next five years. While working capital and net operating profit margin would improve this year as well, these ratios would also continue to strengthen over time. These financial and management changes boost the farm’s financial resiliency, both now and in the future.

- Debt Servicing: 1.43:1

- Working Capital: 104%

- Net operating profit margin: 13%

{kind=link}

{kind=link}

{kind=link}