Rob Saik is excited. He can hardly hold back as he explains the succession plan he used when he sold his own company, Agri-Trend, a few years ago.

Saik had two big goals. As an ag consultant and entrepreneur, he needed financing for his newest venture, the agricultural advisory network called AGvisorPRO, but he also wanted to leave a financial legacy for his family after his death.

Read Also

Celebrating women in agriculture

If you’ve been a long-time reader of Country Guide, you’ll have read many articles in our pages over the years…

“I had done the right thing in setting up a long-term insurance strategy,” Saik says, “But I really needed the money I was paying in premiums to support my new business rather than my legacy. In reality, I wanted both.”

If Saik’s situation sounds familiar, it should. This is exactly the same problem faced by every farmer who wants the next generation to run the family farm, but also wants to leave something behind for non-farming children.

Saik found his solution through his peer group, a group of similar-minded entrepreneurs managed by Strategic Coach, where one of his peers introduced him to 33seven, a wealth creation boutique.

The plan 33seven customized for Saik allowed him to have cash available in his corporation to build his new company, and also provided him with a legacy fund.

A version of this plan can also work for farmers, Saik says. In fact, Saik and 33seven even call it “the farm liquidity solution.”

Part 1: The tax-free zone

Saik is happy to share his solution with any farmer who can use it. “It’s very simple,” he says. “Mom and Dad take out a permanent life insurance policy on themselves.” Generally, he says, “it’s a very large one.”

With the life insurance policy in place, the farm corporation makes premium payments. Insurance payouts can be targeted to non-farming children when the time comes.

Now, to add liquidity. Mom and Dad (and the farm company) can take the life insurance policy to a financial institution and use it as collateral for a loan. The proceeds from this loan make up for the liquidity the farm lost when it made the insurance premiums. The loan money is in place so the farm can continue to grow, and purchase things like fertilizer or farmland.

“Now you’re growing two assets,” Saik says. “You’re growing the farm business and you’re growing the value inside the life insurance policy.”

When Mom and Dad die and the policy pays out, some of the insurance proceeds can repay the company loan and pay estate taxes. The rest can be paid out, tax-free, to the non-farming children.

There’s some degree of urgency to get going on this, Saik says. Mom and Dad must pass a medical exam to qualify for life insurance. “You can’t just kick this down the road forever.”

For over a decade, Saik has been running a peer group for farmers called the PowerFARM program. As these farmers make their own succession plans, the farm liquidity solution is checking a lot of boxes. It provides funds for estate taxes and non-farming kids, and leaves cash in the farm account. In one case, the forced medical exam led a farmer to discover and treat a medical problem he might not have caught otherwise. “The real benefit is not the product, the real benefit is the process,” Saik says.

Don’t say “life insurance”!

Derryn Shrosbree, the founder of 33seven, is at least as excited as Saik to talk about how farmers can benefit from this solution.

Shrosbree moved to Toronto after working on Wall Street and in Tokyo and growing up in South Africa. Since he founded 33seven in 2014, the company has developed succession plans for entrepreneurs in all kinds of sectors. With rising land values and recent high commodity prices, many Canadian farmers are in a position to use these succession plans as well.

Shrosbree knows it’s hard to grab anyone’s attention with the term “life insurance.” People think it’s going to be boring. Or predictable. Shrosbree would rather refer to life insurance by the main benefit it brings to the table: “the tax-free zone.”

“You can use the term “life insurance once,” he said. He was kidding. Sort of. He really doesn’t want farmers to focus on life insurance instead of on the overall picture of this plan. “Life insurance is just a tool. It gets you into what we call the tax-free zone.”

Taxes are the key to this plan. In most cases, the proceeds of life insurance are not taxable. With the right policies in place, investment dollars can grow tax-free inside a life insurance policy.

Shrosbree says this solves problems for farmers who say, “I need estate planning, but I can’t pay for it.” 33seven’s farm liquidity solution uses each dollar twice: first to pay for the insurance policy, then (by using the policy as collateral for a loan) as cash flow within the farm.

“It’s not a loophole, just clever mathematics,” Shrosbree says. “The mathematics is simple. The hard part is having the conversation on the front end.”

This solution is not for everyone. Shrosbree says the solution works best for ultra-high net worth farmers. His definition of “ultra-high net worth” is a farm valued at $30 million or more. If this isn’t your farm, keep reading. Shrosbree says it can still work for what he calls high net worth farmers, with farms worth $10 million or more. And life insurance solutions also work for smaller farms.

So how does this work, exactly? First, a warning. Do not try this without a knowledgeable insurance broker and an accountant who understands farm taxes. Make sure they explain all the risks and potential consequences. This article is only an overview of the main policies and tax laws. Your situation may be different.

Part 2: How can this work?

With apologies to Shrosbree, this next section dives into life insurance. This will be a simple review for many Country Guide readers, so skip ahead if you already understand life insurance as an investment. For anyone who hasn’t given this much thought lately, let’s start with the basics.

Life insurance

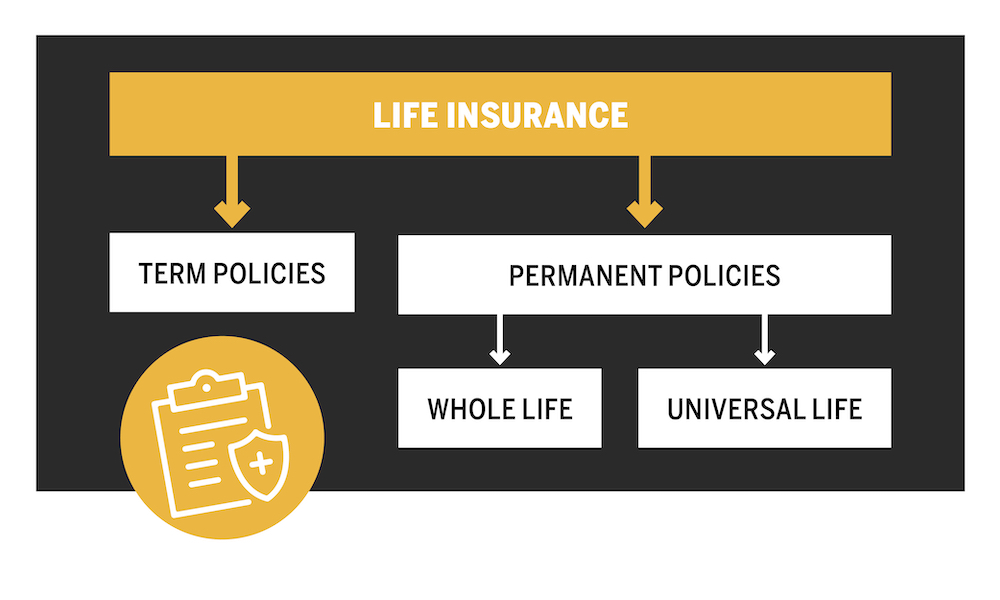

There are two main types of life insurance: term and permanent. Term policies run for a definite length of time, and then they’re finished. Travel insurance is an example of a term type of policy. Once you’re home (healthy) from Mexico, you don’t collect any money, you stop paying premiums, and the policy ends. A parent with young children might buy a term insurance policy scheduled to end when the children are old enough to look after themselves. Term life tends to have cheaper premiums — the insurance company’s actuary calculates the odds of your death and sets your premium to cover the likely cost.

The second type of life insurance is permanent life insurance. Permanent life insurance is the type that applies to 33seven’s farm liquidity solution. Permanent life insurance policies are intended to stay in place for your entire life and then pay out to your beneficiary (or beneficiaries) when you die. As well as a death benefit, permanent life insurance policies usually include an investment component. The two main types of permanent life insurance are whole life and universal.

When you pay your annual permanent life insurance premium, part of the premium covers the insurance company’s actuarial risk — the odds that you might die that year and that they’ll have to pay out your death benefit (let’s say it’s $100,000). The rest of your annual premium is directed into some type of income-earning investment.

Imagine a 45-year-old, Sam, taking out a permanent life insurance policy. If Sam buys a “whole life policy,” annual premiums are usually constant over time. In the early years, the odds of Sam dying are low. Only a small part of the annual payment is needed to cover the risk that he will die and the $100,000 death benefit will come due. Some of Sam’s premium covers that cost, the rest of the premium is invested.

Once Sam is 93 and still paying the same annual premium, more of the annual payment is needed to cover the risk of his death; less is invested.

As Sam ages, the investment component grows. When Sam dies, Sam’s spouse receives the $100,000 death benefit and the investment proceeds.

There are also, usually, other features. If Sam reaches 63 and decides to stop paying premiums and buy a park model trailer in Nevada instead, Sam can ask the insurance company to pay him out the policy’s “cash surrender value,” the CSV. This is the value of the investment that’s built up in Sam’s account over the years.

There are a few major differences between universal and whole life policies. Whole life policies tend to have constant premiums. Universal policies typically offer more flexible premiums, and sometimes policy holders can make changes to the value of the death benefit. There are other differences in the details, and relatively new developments, such as modified whole life premiums. There are also variations such as “last-to-die” or “first-to-die” policies for couples or business partners. This is why you need an insurance broker to find the policy that’s best for you.

Taxes

Taxes are the interesting part of the “farm liquidity solution: Insurance proceeds are tax-free. (Most of the time, in most cases. Please get professional advice.)

In our example, Sam used after-tax dollars to pay the life insurance premiums. After Sam’s death, Sam’s spouse, Sage, gets the insurance payout tax-free.

This works inside a company too. Sam could have bought the life insurance policy through their farm company. After Sam’s death, the life insurance proceeds are paid into the farm’s capital dividend account. As a shareholder, Sage can receive tax-free dividends from this account.

This is where the savings come in. The farm is, presumably, paying the low, small business tax rate, ranging from 9 to 12.2 per cent depending on which province you’re in. The premiums are paid after these low-rate taxes. But Sage can avoid being taxed at a high marginal personal tax rate. Combined federal and provincial marginal tax rates range from 20.05 to 53.53 percent.

Rob Strilchuk is a partner and agricultural tax advisor with MNP, in their Edmonton region. Strilchuk is very enthusiastic about the tax savings farmers can access with life insurance. Basically, he says, “It’s like a corporate tax-free savings account.”

As with all good things, there are caveats. Depending on the type of policy you have, it may not be possible to pay out the entire investment portion of your policy to shareholders tax-free (though the death benefit will always be tax-free). The tax-free portion of investments is based on the type of policy you have and how you fund it.

By adding a few extra steps, farmers setting up their own insurance policies can make sure the insurance payouts end up in the right pockets.

Consider a farmer with two children. The intention is for one child to take over the farm and the other to receive $1 million from an insurance policy.

“Ahead of time,” Strilchuk says, “Set it up so that the company has common shares, and a class of preferred shares.” The common shares are the controlling shares owned by the child running the farm. The non-farming child can hold preferred shares. The two siblings can sign a shareholders’ agreement where the farming child agrees to purchase the preferred shares for $1 million upon the death of the parent. When the policy pays out into the farm’s capital dividend account, the non-farming sibling can receive the payment in non-taxable dividends.

Adding liquidity

You don’t need to use the next step. You can stop reading right now and still use the tax savings feature of life insurance. But much of Rob Saik’s enthusiasm comes from the next step: using the life insurance policy as collateral for a loan.

Financial institutions are generally quite comfortable using permanent life insurance policies as collateral. Everyone dies eventually.

The loan allows your farm company to buy an insurance policy, and still have cash in the farm account.

To make this more attractive, two of these expenses may be tax deductible: the interest paid on the loan, and a portion of the insurance premiums.

The interest portion of the loan payment is generally a deductible expense, but the CRA has a policy of “interest traceability.” Loan proceeds must be kept within the company and be used by the company. The CRA may scrutinize this, Strilchuk says, “if you’re using a company asset as security for a personal loan.”

So, if the borrowed money is used to buy something like farmland or fertilizer, interest costs are generally deductible. But if the borrowed money is withdrawn from the company so your brother can buy a boat, the CRA will not allow the interest expense.

As for deducting a portion of the premium payments, get professional advice before purchasing a life insurance policy. Remember that the annual premiums include two components: the actuarial insurance component and the investment component. Insurers call the actuarial cost the “Net Pure Cost of Insurance,” or NPCI. Each year, the lesser of your actual insurance premium, or your NCPI may be a tax-deductible expense.

Other benefits

MNP’s Rob Strilchuk is on board with the concept of permanent life insurance for farmers. Sometimes, he says, the rates of return from insurance investments can be higher than other safe investments, such as GICs, and the tax-free component definitely makes insurance attractive.

As well as providing tax-free benefits to off-farm children, Strilchuk points out that using life insurance can allow farmers to avoid estate settlement costs (also known as probate fees). These fees vary by province; in Saskatchewan, probate is necessary if the deceased owns land. The fees are $7 on every $1,000 of estate assets (or 0.7 percent), large enough to bother avoiding.

Why isn’t everyone doing this?

As Shrosbree warned, this might be because people don’t want to talk (or read) about life insurance. Strilchuk thinks so. “The minute you mention life insurance,” Strilchuk says, “people lose interest. It’s something that a lot of farmers think doesn’t apply to them.”

Wayne Paproski is another partner at MNP and part of MNP’s national transaction tax service team. Paproski agrees that using life insurance policies for tax and succession planning “is generally underutilized in private companies, including farming,” even though “it can accomplish a lot of good things,” such as debt repayment, paying estate taxes, or leaving a legacy for non-farming children.

Some people overlook insurance because, in the past, “somebody in their family or community was burnt by an insurance salesman,” Paproski says. Maybe they were overpromised when they purchased a policy, or maybe they bought a policy that wasn’t the right fit. Get a referral to the right broker.

Strilchuk also reiterates the warning from Rob Saik — if you’re going to do this, don’t wait too long. “The minimum amount of time it will take to place this is about six months,” Strilchuk says. It will take time to get a health check and to get quotations.

Part 3: Risks & tips

Dean Klippenstine is a Regina-based partner and agriculture business advisor with MNP. Klippenstine agrees that this solution can do exactly what Saik and Shrosbree want it to do. But he does warn that when young people implement this plan, the insurance policy could be in place for a long time. Over the years, the underlying variables can change significantly. For example, the interest rates your company pays to borrow money to pay premiums could change quite a bit while a farmer ages from 40 to 70. Tax rates might also change, making insurance less (or more) attractive.

The risks of leverage

Klippenstine also warns against “aggressive leverage.” Borrowing money based on insurance can add substantial risk to a succession plan.

MNP’s Paproski says farmers can reduce risk and still save on taxes by not taking out a loan against the policy to make premium payments. Instead, he says, think of the possibility of getting a loan as a potential for more flexibility. For example, if a “section of land across the road comes up, you can access that money through a loan.”

Another way to look at this is to see the policy as one of several assets owned by the farm. If the farm needs a loan, it could leverage that asset, or use another asset, such as land, as collateral.

Paproski sees potential for success with this strategy in cases where farm managers understand the costs and benefits, have fully committed to making the premium payments over the life of the policy, and “they’re comfortable making that commitment.”

These farmers, he says, are willing to buy the policy without taking out a loan against it. “The debt is just a feature you may or may not choose to use.”

Stick with the plan!

Another potential risk is that future farm managers may stop paying the insurance premium and take the cash surrender value (CSV). Maybe they didn’t fully agree with this tactic in the first place, or maybe they don’t see the benefits. Or maybe a short-term cash-flow issue makes it hard to pay the premiums.

Sometimes, Paproski says, “clients get to be elderly, and ask ‘Why do I have a loan for $5 million?’”

First, a portion of the CSV payout will be taxable. Then, to make it worse, the taxable portion will not be taxed at the low small-business tax rate. The CRA will classify it as “inactive” income and tax it at a higher rate. This rate varies by province, but, Poproski says, “it’s generally around 50 percent or higher.”

There are formulas for calculating the taxable amount of your CSV in any given year — ask your broker to explain how taxes would affect your specific policy. In general, in the early years of your policy, the taxable portion will be lower, but the CSV will also be lower. As your CSV grows, the taxable portion also grows.

Keep your estate qualified

Paproski recommends working with accountants and tax professionals to confirm the plan works with other important estate planning issues. For example, the CRA has rules around the lifetime capital gains exemption that gives most farmers an exemption on $1.25 million in capital gains (as increased from $1 million in the 2024 federal budget). One rule is that, for shares of your farm to qualify for the exemption, your farm must be a “qualified small business.” To qualify, 90 percent of the fair market value of your farm assets must be actively used for farming.

Consider the death of a major shareholder. The life insurance proceeds are deemed to be paid to the farm immediately. Will this payout be less than 10 percent of the fair market value of the rest of the assets (land, machinery), or will the cash payment tip your farm over the scales and out of the “qualified small business” category? This is a question for your accountant and your insurance broker.

There are many other tax and estate factors to consider. As Paproski says, “all these levers are moving at once.” But with the right advice, it can work for you. “It’s no problem as long as someone’s watching, and they know what they’re watching for.”

Part 4: Get good advice

Before you do this, find an insurance broker with the experience and ability to give you the best advice. Strilchuk describes these brokers as “high-end life insurance agents.”

Advisors at banks have access to life insurance products, but they may receive a commission or benefit from promoting the bank’s in-house products. These might not be the best products for you. Some brokers are limited to selling policies from only one company; others can sell products from more than one.

As well as working with a good broker, Strilchuk recommends working with a reliable insurance company, ideally one of the top three to five biggest insurance companies in Canada. Remember, he says, “it might be 20 years before it pays out.” Make sure your insurer will still be there after you aren’t.

In the past, insurance investment options were more limited, Strilchuk says, but new types of insurance investments have come into play in recent years. Now, he says, “you decide where you want to put your money.”

So this can work? Yes, but maybe not for everyone, so before you try it, hire a good team of experts.

“This seems too good to be true,” Paproski says. Earlier in his career, he didn’t appreciate the value of insurance. But now, he says, “after a deep dive, I was a convert.” He believes 33seven’s farm liquidity solution can work for some farmers, as long as they “make an informed risk decision.”

And don’t forget that people are always at the heart of farm transition and life insurance. This plan can’t possibly work unless your family can have open and honest discussions about the future of the farm.

Saik agrees. “The hardest part in the whole equation is the conversation.”